Exponential Regression using Newton’s Method

We now show how to create a nonlinear exponential regression model using Newton’s Method.

Property 1: Given samples {x1, …, xn} and {y1, …, yn} and let ŷ = αeβx, then the value of α and β that minimize

![]()

![]()

Proof: For a proof using calculus, click here

Property 2: Under the same assumptions as Property 1, given initial guesses α0 and β0 for α and β, let F = [f g]T where f and g are as in Property 1 and

Now define the 2 × 1 column vectors Bn and the 2 × 2 matrices Jn recursively as follows

![]()

![]()

![]()

Then provided α0 and β0 are sufficiently close to the coefficient values that minimize the sum of the deviations squared, then Bn converges to such coefficient values.

Proof: For a proof using calculus, click here

Property 3: The approximate covariance matrix for the coefficients vector is given by

![]()

where![]()

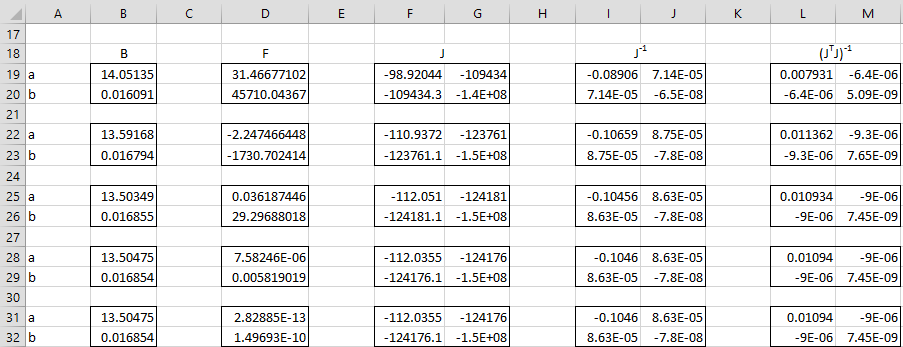

Example 1: We now show how to calculate the value of the α and β coefficients for the exponential regression model for the data in Example 1 of Exponential Regression using a Linear Model or Exponential Regression using Solver (repeated in range A3:B14 of Figure 0), this time using Newton’s Method (i.e. Property 2).

Figure 0 – Data for Example 1

The first 5 iterations of Newton’s method are shown in Figure 1. As you can see the coefficients calculated in step 5 (range B31:B32) are the same as those in step 4 (range B28:B29) and so convergence is reached after 5 steps, with values α = 12.50475 and β = .016854.

Figure 1 – Exponential Regression using Newton’s Method

In Figure 2 we show key formulas used in Figure 1 based on Property 1 and 2 and referencing the input X data in range A4:A14 and Y data in range B4:B14 from Figure 1 of Exponential Regression using Solver.

| Item | Cells | Formula |

| B0 | B19:B20 | use values from Excel exponential regression |

| F0 | D19 | =SUMPRODUCT(SUMPRODUCT($B$4:$B$14-B19*EXP(B20*$A$4:$A$14),EXP(B20*$A$4:$A$14))) |

| D20 | =B19*SUMPRODUCT(SUMPRODUCT($B$4:$B$14-B19*EXP(B20*$A$4:$A$14),EXP(B20*$A$4:$A$14),$A$4:$A$14)) | |

| J0 | F19 | =-SUMPRODUCT(EXP(2*B20*$A$4:$A$14)) |

| G19 | =SUMPRODUCT(SUMPRODUCT($B$4:$B$14-2*B19*EXP(B20*$A$4:$A$14),EXP(B20*$A$4:$A$14),$A$4:$A$14)) | |

| F20 | =G19 | |

| G20 | =B19*SUMPRODUCT(SUMPRODUCT($B$4:$B$14-2*B19*EXP(B20*$A$4:$A$14),EXP(B20*$A$4:$A$14),$A$4:$A$14^2)) | |

| J0-1 | I19:J20 | =MINVERSE(F19:G20) |

| B1 | B22:B23 | =B19:B20-MMULT(I19:J20,D19:D20) |

Figure 2 – Formulas from Figure 1

We can now create the regression analysis as shown in Figure 3.

Figure 3 – Exponential Regression results using Newton’s Method

Key formulas are shown in Figure 4, referencing the cells in Figure 1.

| Item | Cells | Formula |

| α coefficient | P25 | =B31 |

| β coefficient | P26 | =B32 |

| α s.e. | Q25 | =SQRT(L31*R21) |

| β s.e. | Q26 | =SQRT(M32*R21) |

| SSE | Q21 | =SUMPRODUCT((B4:B14-B31*EXP(B32*A4:A14))^2) |

| MSE | R21 | =Q21/P21 |

Figure 4 – Formulas from Figure 3

Observation: The following is an alternative approach for finding the regression coefficients α and β. By Property 1

![]()

Thus, if α ≠ 0 we can solve for α to get

![]()

Thus the original two equations in two unknowns can be replaced by the following equation in one unknown:

![]()

This can be solved iteratively using Newton’s Method in one variable, as described in Newton’s Method.

Observation: There is another algorithm that is commonly used to find the regression coefficients called the Levenberg-Marquardt algorithm, which combines the advantages of Newton’s Method with those of the algorithm used by Solver. We won’t consider this algorithm further here.